JPMorgan Equity Premium Income ETF (JEPI) has deviated completely from the broader US stock market. It has dropped by over 5.90% from its highest point this year, even as the S&P 500, Dow Jones, and Nasdaq 10o hover at their all-time highs. This performance is a sign that the fund’s 8% yield is a value trap.

How JEPI ETF works

JEPI, the biggest player in the covered call ETFs, gained popularity a few years ago because of its strong yield. For a long time, it has offered a monthly dividend with an annual yield of over 8%. This yield is much more than what the S&P 500 Index and other popular dividend ETFs like SCHD and VYM pays. It is also higher than what government bonds are paying.

The fund promises its investors access to this yield and access to some of the biggest companies in the United States, including popular names like NVIDIA, Microsoft, Meta Platforms, and Google. In other words, it offers the best of both worlds in terms of its dividend payouts and stock returns.

JEPI achieves this by using the covered call strategy. This approach involves buying the individual stocks in the portfolio, and then selling its calls. By doing that, it benefits as these stocks rises, and takes a premium, which it returns to its holders as a monthly dividend.

Is the JEPI dividend worth it?

Still, analysts warn that JEPI and other covered call ETFs are yield traps as their total returns are usually not all that attractive. In other words, it may pay a high dividend, but its performance always lags behind that of the benchmark assets.

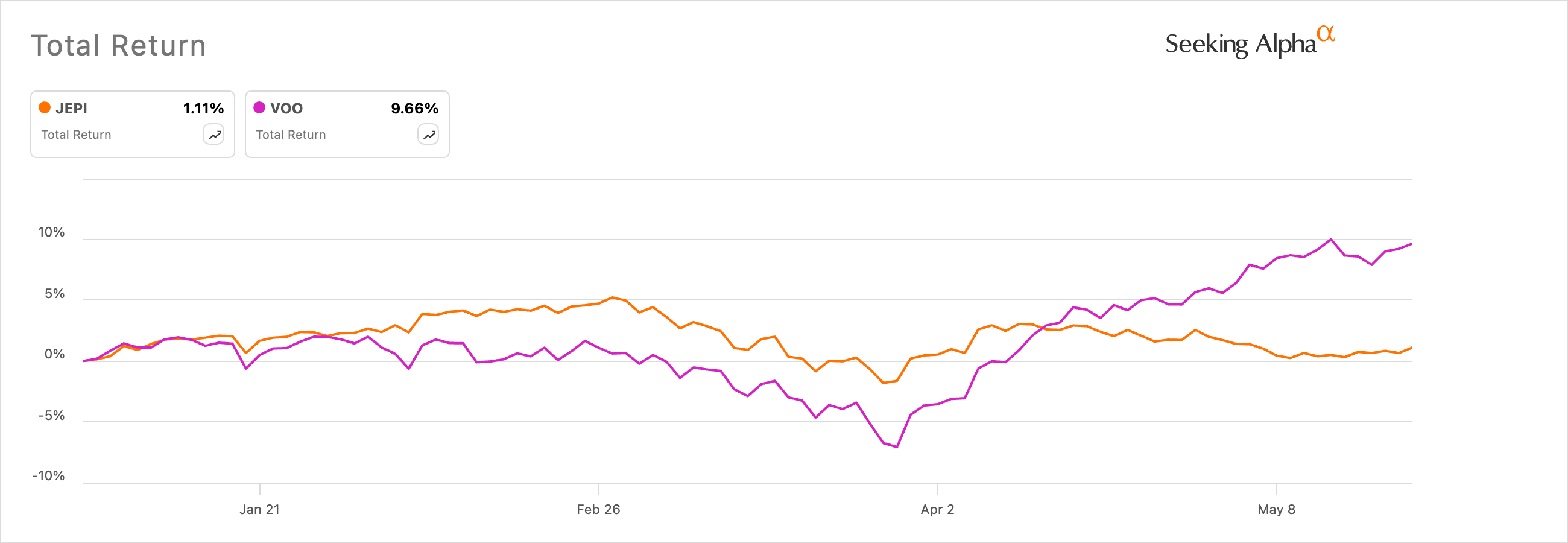

For example, data shows that JEPI’s total return this year is just 1.1%, while the S&P 500 Index has returned nearly 10%.

JEPI vs VOO ETF | Source: SeekingAlpha

The same is true when you compare other covered call ETFs. A good example of this is JEPQ, JEPI’s sister that tracks the Nasdaq 100 Index. JEPQ ETF has returned 7.50% this year, while the Nasdaq 100 Index jumped by nearly 17%.

The main reason for this is how these covered call ETFs work. As mentioned, the fund managers buys assets, and then sells call options on the same.

A call option gives a fund manager a right, but not the obligation to buy an asset before an expiry period. In this case, the fund benefits when the underlying asset is rising up to a certain point.

For example, if it rises above the strike price, as the S&P 500 Index is doing, it misses the whole rally. This explains why the fund always underperforms when the index is in a bull run.

The same happens across most covered call ETFs, except in bear markets. However, in those markets, their edge is usually not all that strong. For example, the CONY ETF, which yields over 80%, has had a total return of minus 17% this year, while Coinbase stock has dropped by 18%.

READ MORE: JEPI ETF yields 7.5% while VOO yields 1.15%: better buy?

The post JEPI ETF stock is falling as the S&P 500 soars: is the 8% yield an illusion? appeared first on Invezz