The private credit industry, one of the fastest-growing corners of global finance over the past decade, is facing an unexpected stress test as investors attempt to withdraw billions of dollars from funds that helped fuel its expansion.

Rising redemption requests across several large private credit vehicles have forced fund managers to impose limits on withdrawals, sell assets and even inject their own capital to stabilise investor sentiment.

The developments are raising concerns that the model that powered the industry’s explosive growth—especially its increasing reliance on wealthy individual investors—may be encountering its first major challenge.

While the sector is far from a full-blown crisis, the surge in withdrawal requests is exposing the tensions inherent in offering periodic liquidity to investors while holding loans that are designed to remain locked up for years.

Cliffwater and Morgan Stanley become latest to cap redemptions

The latest sign of strain came when Cliffwater, a major private credit manager, told clients that investors in its largest fund requested to redeem 14% of their holdings during the latest quarter.

The $33 billion fund will only be able to meet about half of those requests, meaning the remaining investors will need to wait until at least the next quarter to withdraw their money.

Morgan Stanley has also faced similar pressures.

It’s North Haven Private Income Fund, which manages nearly $8 billion in assets, returned roughly $169 million to investors after limiting withdrawals to 5% of total shares during the latest redemption window.

In a letter to clients, Morgan Stanley said the decision to cap withdrawals was intended to prevent forced asset sales during periods of market volatility and to preserve long-term returns.

The measures reflect a growing dilemma for private credit funds as redemption requests rise.

Managers must balance the need to satisfy investors seeking liquidity against the risk that selling loans too quickly could erode the value of their portfolios.

From Blue Owl to BlackRock: rising redemption requests signal investor unease

It all started in February when Blue Owl Capital announced it would permanently restrict withdrawals from one of its retail-focused debt funds.

Instead of allowing investors to redeem their money on a quarterly basis, the firm said it would shift to periodic payouts funded by asset sales, earnings and strategic transactions.

Blue Owl also said it plans to sell about $1.4 billion worth of loans held across three funds to a group of large pension and insurance investors.

Those worries spread further when reports emerged that Blackstone Private Credit, the business development company known as BCRED, faced $1.7 billion in net withdrawals during its latest fiscal quarter.

Gross redemption requests exceeded the fund’s 7% quarterly limit.

To manage the outflows without triggering prorated payouts to investors, Blackstone adopted an unusual solution.

The firm and its employees injected $400 million into a feeder fund that channels investments into BCRED, effectively offsetting the redemption pressure and allowing the fund to meet withdrawal requests.

Then, BlackRock recently limited redemptions from its $26 billion HPS Corporate Lending Fund after investors sought to withdraw 9.3% of shares in the first quarter, far exceeding the fund’s 5% quarterly cap.

The incident marked the first time withdrawal requests breached that limit.

“You’re seeing a crisis of confidence,” Victor Hong, a former investment banking risk executive, said in a report by the New York Times.

Investor psychology also appears to be playing a role.

Wealth advisers say concerns about liquidity can quickly become self-reinforcing once investors fear they may not be able to access their money quickly.

“Anytime somebody hears that other people are getting out, you don’t want to be last,” said Steve Curley, co-managing principal at 55 North Private Wealth in the NYT report.

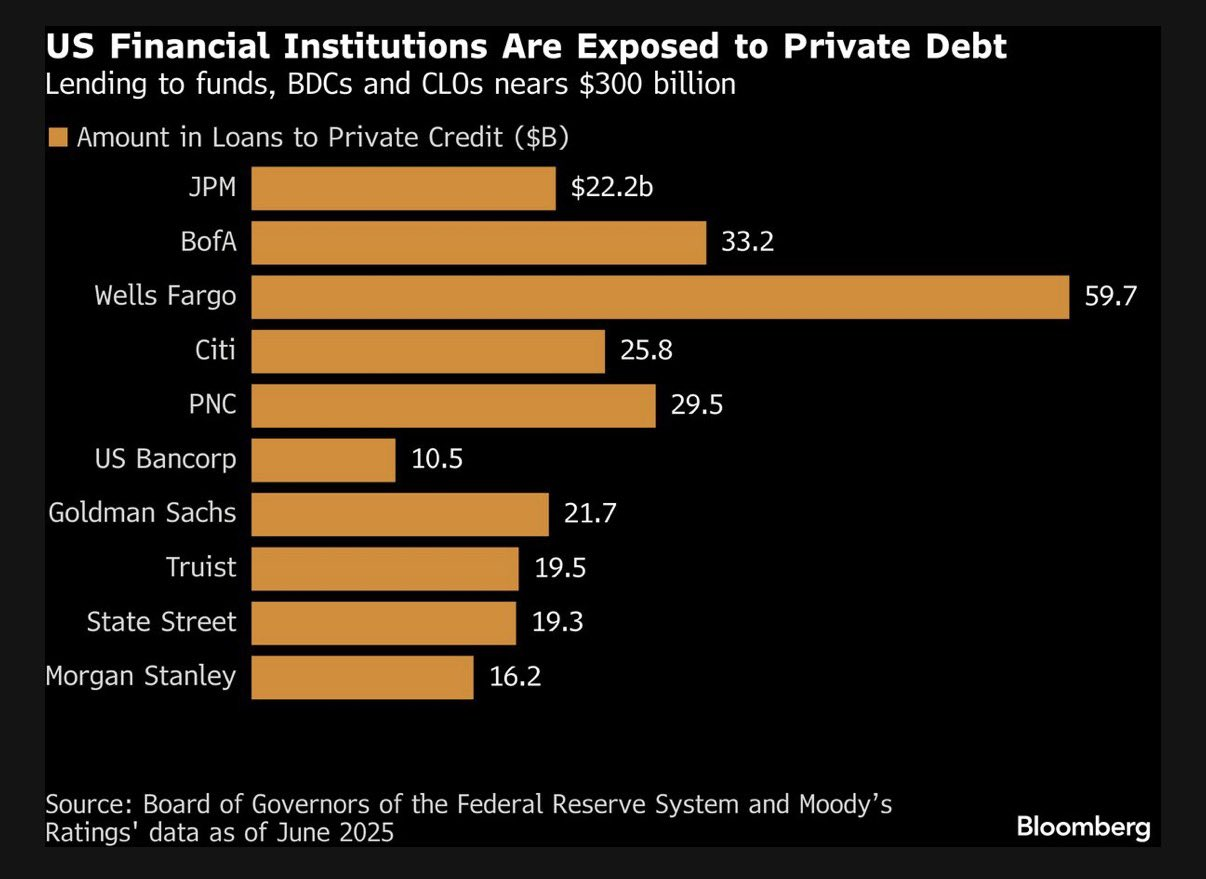

Banks grow cautious on lending

Concerns about the health of some private credit portfolios are also prompting caution among banks that provide financing to these funds.

JPMorgan Chase has reportedly begun restricting lending to certain private credit funds after marking down the value of loans tied to software companies, according to a report by the Financial Times.

The markdowns come as the technology sector faces increased scrutiny from investors, particularly amid uncertainty about how advances in artificial intelligence could reshape business models and valuations.

Source: Bloomberg

JPMorgan chief executive Jamie Dimon had earlier warned that more problems could emerge within the opaque world of private lending.

Dimon said last year that the market could reveal more “cockroaches,” a term used in finance to describe how the discovery of one issue often signals that others may soon follow.

Although the bank’s asset markdowns do not necessarily signal a systemic crisis, they suggest that the easy assumptions that supported the private credit boom—around valuations, liquidity and underwriting—may be coming under closer examination.

Understanding private credit’s rapid rise

Private credit refers to loans provided by non-bank lenders directly to companies, typically small and mid-sized businesses that fall below investment-grade credit ratings.

These loans are usually negotiated privately between lenders and borrowers and are not traded on public markets.

As a result, they often involve customised terms tailored to each borrower’s needs.

Direct lending, the most common form of private credit, generally involves senior secured loans with floating interest rates.

Because these loans are not easily traded, lenders usually hold them until maturity or until the borrower refinances.

The absence of a liquid secondary market means investors cannot easily sell their positions if they want to exit quickly.

“The feature, or the bug, of these things is you can’t get out right away,” Matthew Malone, head of investment management at Opto Investments said in a Morningstar report.

“Because of that, the client is getting reminded every quarter or month that this thing is still not resolved.”

Retail investors become a key funding source

Historically, private credit funds were primarily backed by large institutional investors such as pension funds, insurance companies, sovereign wealth funds and family offices.

These investors typically accepted long lock-up periods in exchange for higher returns and diversification.

Over the past decade, however, the industry has expanded rapidly.

Assets in private credit funds have grown to more than $3 trillion globally, prompting firms to seek new sources of capital.

This is why private credit firms have increasingly turned to wealthy individuals and retail investors to fuel further expansion.

Several firms also seek access to the vast pool of retirement savings held in 401(k) plans.

From Cliffwater to Apollo Global Management, BlackRock, Blackstone and Blue Owl Capital, all marketed their funds to individual investors.

They launched a range of investment vehicles, such as business development companies and interval funds, designed to make private credit more accessible to individual investors.

These products generally promise periodic liquidity, allowing investors to request withdrawals every quarter or at regular intervals.

In practice, however, the underlying loans often remain locked up for several years.

The structure worked smoothly as long as new investor money continued flowing into the funds.

Fresh inflows could be used to meet redemption requests without requiring managers to sell existing loans.

But as market conditions shift and investor sentiment turns cautious, the mismatch between liquid redemption promises and illiquid loan portfolios is becoming more visible.

If too many investors attempt to withdraw their money simultaneously, funds may have little choice but to impose limits on redemptions.

“With any market that’s growing rapidly, there can be some level of a shakeout,” said Scott Adelson, chief executive officer of Houlihan Lokey, whose private credit database and analytical platform aggregates data from more than 60,000 loan valuations.

“There are some credit providers that could have a difficult time.”

Managers face a difficult balancing act

The current wave of redemption requests is forcing fund managers to confront a difficult decision.

They can loosen withdrawal limits to satisfy investors seeking liquidity, which may require selling assets quickly and potentially damaging portfolio performance.

Alternatively, they can maintain strict redemption caps and “gate” withdrawals, a move that may protect portfolio value but risks alarming investors and reducing future inflows.

A similar backlash occurred in 2022 when withdrawals were capped at Blackstone’s real estate income trust, a non-traded property fund widely held by wealthy individuals.

Industry observers say a prolonged period of redemption pressure could have broader implications for the private capital ecosystem.

If funds are forced to sell large volumes of loans to meet withdrawal demands, the market could face downward pressure on prices.

That, in turn, might affect valuations across the sector.

Economists also warn that stresses in private credit could intersect with vulnerabilities elsewhere in financial markets.

Mohamed El-Erian, an economist and former chief executive of Pimco, recently noted that early warning signs are beginning to appear.

“This week’s news from private credit markets echoes Jamie Dimon’s warning about cockroaches,” El-Erian said.

He added that while the developments do not yet suggest systemic risk, investors should monitor how private credit interacts with other potential market excesses, including the rapid expansion of artificial intelligence-related investments and vulnerabilities in global bond markets.

Debate continues over the industry’s resilience

Despite the rising concerns, some industry participants argue that the turbulence reflects a misunderstanding of how private credit funds are structured rather than a fundamental problem with the asset class.

Don Calcagni, chief investment officer at Mercer Advisors, said in the Morningstar report that the underlying loan portfolios across the industry remain broadly healthy.

According to Calcagni, much of the current tension stems from investors who may not have fully appreciated the illiquid nature of the investments when they entered the funds.

The coming months will likely test that argument.

“It seems unlikely that there’s going to be a spiral in terms of a credit crunch” as long as the US economy is doing reasonably well and the Federal Reserve is inclined to cut rates or stay on hold,” Christian Stracke, president at the $2.3 trillion asset manager Pacific Investment Management Co. or Pimco, said in a Bloomberg report.

But “if you’re in the more problematic loans, whether they’re private or traded bank loans, then it’s going to be very difficult for that borrower to refinance themselves,” he said.

Wealth advisers and institutional investors are closely watching how private credit managers navigate the surge in redemption requests and whether investor confidence stabilises.

Some analysts say it could take more than a year for certain investors to fully exit funds if withdrawal caps remain in place.

If redemption pressures persist, the sector could face slower inflows, tighter financing conditions and a more cautious approach to lending.

For an industry that thrived on rapid growth and abundant capital, the current period may mark a turning point—one in which investors begin to reassess the risks associated with assets that promise attractive returns but offer limited liquidity.

The post As investors seek exits, is private credit’s liquidity model breaking? appeared first on Invezz